Higher education in India is no longer affordable for the average middle-class family without financial planning. Tuition fees at private universities have surged, overseas education costs are touching ₹40–50 lakh for many programs, and even public institutions have revised their fee structures. That is exactly why Education Loan Finance in India 2026 has become one of the most searched topics among students and parents this year. The lending environment has changed rapidly, and if you do not understand how Education Loan Finance In India 2026 works today, you could end up signing a loan that becomes a long-term burden. Students are no longer just comparing colleges they are comparing loan interest rates, repayment flexibility, moratorium clauses, and subsidy eligibility. Education Loan Finance in India 2026 is more structured, more digital, and more credit-driven than ever before. Banks are evaluating employability, university ranking, and co-applicant financial strength before approving funds. Whether you are planning to study in India or abroad, understanding the latest rules can save you lakhs in repayment.

Education Loan Finance In India 2026 reflects a shift toward transparency, digital processing, and stricter credit evaluation. Lenders are not simply funding degrees anymore; they are assessing future income potential. Public sector banks have aligned most education loans with repo-linked floating interest rates. Private banks are offering faster approvals but often at slightly higher rates. NBFCs are filling gaps for students who may not qualify under traditional bank criteria. Meanwhile, government subsidy schemes continue to support economically weaker sections, though verification has become more digital and data-driven. If you want better terms in Education Loan Finance In India 2026, you need strong documentation, a reliable co-applicant credit profile, and a realistic repayment strategy.

Table of Contents

Education Loan Finance in India 2026

| Change Area | What Has Changed In 2026 | What It Means For Students |

|---|---|---|

| Interest Rate Structure | Repo-linked floating rates dominate & fixed rates are limited | EMIs may increase or decrease depending on RBI policy |

| Maximum Loan Limit | Higher caps for overseas programs & premium institutions | Greater access to large funding amounts |

| Collateral Policy | Stricter valuation process & legal verification | Better documentation required before approval |

| Moratorium Rules | Limited extensions & encouragement of partial payments | Early planning reduces interest burden |

| Credit Assessment | Higher weightage to co-applicant CIBIL & income stability | Parent’s financial profile directly impacts approval |

| Government Subsidy | Digitally tracked income verification & direct benefit transfers | Faster but stricter eligibility checks |

| Loan Processing | Fully digital applications & video KYC systems | Faster sanction timelines |

Education Loan Finance In India 2026 offers more funding opportunities than ever before, but it also demands smarter financial planning. Higher loan limits, digital processing, and subsidy schemes have improved access. At the same time, lenders are stricter about credit evaluation and repayment capacity. Before signing any agreement, evaluate floating rate risk, calculate total repayment under different scenarios, and ensure your co-applicant’s financial profile is strong. An education loan can unlock life-changing opportunities but only if managed wisely.

1. Interest Rates Are Now More Dynamic

One of the biggest shifts in Education Loan Finance In India 2026 is the strong move toward repo-linked lending rates. Most public sector banks now calculate education loan interest rates based on the RBI’s repo rate.

What this means in practical terms:

- If the RBI raises the repo rate, your interest rate increases.

- If the repo rate falls, your EMI may reduce.

- Floating rates are far more common than fixed rates in 2026.

Current education loan interest rates typically range between 8.5% and 13%, depending on the lender and borrower profile. Even a small rate fluctuation of 0.5% can impact your total repayment by lakhs over a 10–15 year tenure. That is why borrowers must calculate repayment under multiple rate scenarios.

2. Higher Loan Limits For Overseas Education

Indian students studying abroad have reached record numbers, and lenders have expanded funding limits accordingly. Under Education Loan Finance In India 2026, several banks now offer loans up to ₹1.5 crore for top global institutions.

However, higher loan limits come with stricter evaluation. Banks assess:

- University ranking

- Course employability

- Expected starting salary

- Co-applicant income stability

For countries like the US, UK, Canada, and Australia, approval rates are higher if the university is ranked well and the course has strong employment outcomes.

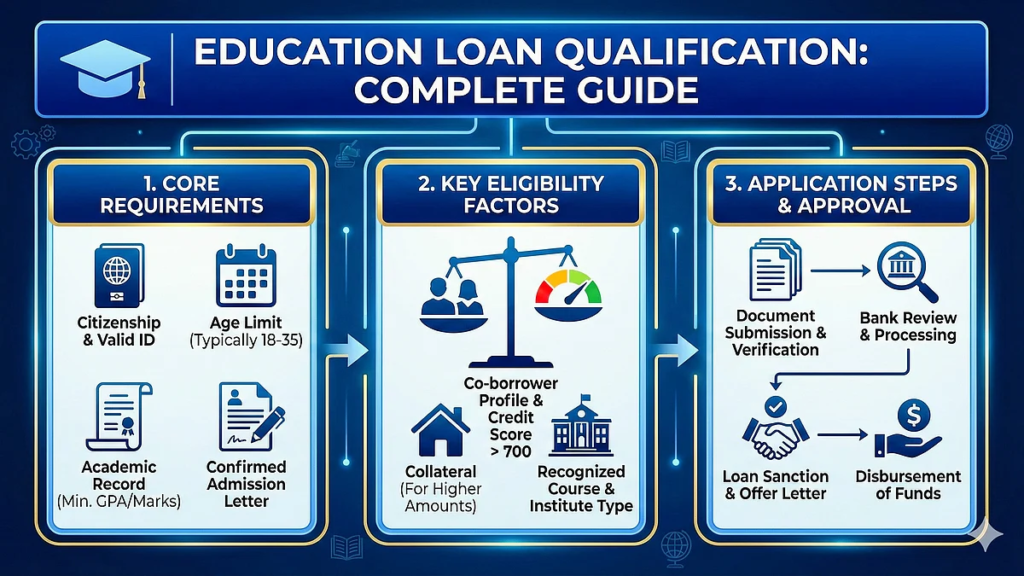

3. Collateral Requirements Have Tightened

For loan amounts above ₹7.5 lakh to ₹10 lakh, collateral is often required. In Education Loan Finance In India 2026, property verification processes have become more detailed.

Commonly accepted collateral includes:

- Residential property

- Fixed deposits

- Government bonds or securities

Banks now conduct deeper legal checks and valuation assessments. Incomplete paperwork can delay sanction letters. If you are planning to pledge property, begin documentation early to avoid last-minute issues.

4. Greater Focus on Co-Applicant Credit Score

This is one of the most critical changes in Education Loan Finance In India 2026. Since students typically do not have a credit history, lenders rely heavily on the co-applicant, usually a parent or guardian.

In 2026:

- A CIBIL score above 700 improves approval chances.

- High existing EMIs reduce eligibility.

- Stable income documentation is mandatory.

If the co-applicant has past loan defaults or poor repayment history, lenders may either reject the application or increase the interest rate.

5. Moratorium Periods Are Becoming More Structured

The traditional moratorium structure of course duration plus 6–12 months still exists. However, lenders now discourage complete payment holidays.

In Education Loan Finance in India 2026:

- Students are encouraged to pay simple interest during study years.

- Some banks promote partial EMI payments during internships.

- Extensions beyond the standard grace period are harder to obtain.

Allowing interest to compound over a four-year course can significantly raise the principal amount. Paying even small amounts early can reduce long-term burden.

6. Expansion Of Government Subsidy Schemes

Government interest subsidy schemes continue in 2026, especially for economically weaker families. The verification system has become fully digital.

Key features include:

- Income-based eligibility checks

- Direct benefit transfer mechanisms

- Centralized monitoring systems

If eligible, students receive interest subsidy during the moratorium period, which lowers the overall repayment amount.

7. Fully Digital Loan Processing

Loan processing has become largely paperless in 2026. Most banks now offer:

- Online application forms

- Digital document uploads

- Video KYC verification

- Faster sanction approvals

Approval timelines that once took weeks can now be completed within days. However, faster processing does not mean you should skip reviewing terms. Always read the loan agreement carefully.

Public Sector Banks Vs Private Banks Vs NBFCs

Choosing the right lender can impact both interest rates and flexibility.

Public Sector Banks

- Generally lower interest rates

- Government-backed policies

- Slightly longer processing time

Private Banks

- Faster approval systems

- Flexible repayment options

- Competitive but slightly higher rates

NBFCs

- Higher approval chances for unconventional profiles

- Faster disbursal

- Higher interest compared to banks

In Education Loan Finance In India 2026, comparing total repayment cost not just EMI is crucial.

Hidden Costs Students Must Watch

Many borrowers focus only on the interest rate. That is not enough.

Check for:

- Processing fees ranging from 0.5% to 1%

- Legal and valuation charges

- Insurance premiums

- Prepayment penalties

- Late payment fees

For example, a 1% processing fee on a ₹25 lakh loan means ₹25,000 upfront. These additional costs should be factored into your decision.

How To Prepare Before Applying

Preparation can significantly improve approval chances.

Follow this checklist:

- Compare at least three lenders.

- Check co-applicant CIBIL score before applying.

- Use EMI calculators for different rate scenarios.

- Understand total repayment over full tenure.

- Confirm eligibility for subsidy schemes.

Well-prepared applicants often secure better negotiation power.

Smart Borrowing Tips For Students

- Borrow only what you genuinely need.

- Avoid stretching to maximum eligibility unless required.

- Pay simple interest during the study period if possible.

- Keep track of repo rate movements.

- Maintain communication with your lender after graduation.

Education Loan Finance In India 2026 rewards financially aware borrowers who plan early.

Read More:-

FAQs

1. What Is the Average Interest Rate For Education Loans In 2026?

Interest rates generally range between 8.5% and 13%, depending on lender type, loan amount, and credit profile.

2. Is Collateral Mandatory for Education Loans?

Collateral is usually required for higher loan amounts, particularly for overseas education beyond ₹7.5–10 lakh.

3. How Important Is the Co-Applicant’s Credit Score?

Extremely important. A CIBIL score above 700 significantly improves approval chances and may reduce interest rates.

4. Can I Get an Education Loan Without Income Proof?

It is difficult. Most lenders require income proof from the co-applicant unless covered under specific government-backed schemes.