India’s retirement savings system has always been built around security and long-term stability. Among the many government-backed savings schemes available to salaried employees, the Voluntary Provident Fund remains one of the most trusted options. Recently, the government decided to keep the VPF rate at 8.25%, a move that reassures millions of employees who depend on provident fund savings to build their retirement corpus. For investors who value safety and predictable returns, the VPF rate at 8.25% continues to offer a dependable investment avenue. However, the announcement has also sparked a wider discussion among investors and financial experts. While the VPF rate at 8.25% is relatively attractive compared with many traditional fixed-income options, some investors are wondering whether it is enough in today’s changing financial environment. Rising inflation, increased awareness of diversified investments, and easy access to equity markets are making investors rethink their strategies. As a result, many are asking an important question: should VPF remain the primary retirement investment or simply one part of a broader financial plan?

The VPF rate at 8.25% is currently one of the highest interest rates offered by a government-backed savings scheme in India. The Voluntary Provident Fund allows salaried employees to contribute more than their mandatory Employees’ Provident Fund contribution to increase their retirement savings. Since VPF is an extension of EPF, the same interest rate declared by the Employees’ Provident Fund Organisation applies to both schemes. For individuals looking for safe and long-term wealth accumulation, the VPF rate at 8.25% provides an appealing combination of reliability and tax benefits. Unlike market-linked investments that fluctuate daily, the VPF rate at 8.25% ensures consistent annual growth, making it a preferred option for risk-averse investors.

Table of Contents

India Keeps VPF Rate At 8.25%

| Key Aspect | Details |

|---|---|

| Scheme Name | Voluntary Provident Fund |

| Current Interest Rate | 8.25% |

| Managed By | Employees’ Provident Fund Organisation (EPFO) |

| Risk Level | Very Low (Government-backed) |

| Interest Type | Compounded Annually |

| Tax Benefits | Eligible Under Section 80C |

| Lock-in Period | Until Retirement Or Job Change |

| Contribution Limit | Up To 100% Of Basic Salary & Dearness Allowance |

| Ideal For | Long-Term Retirement Savings |

| Investment Category | Fixed Income Retirement Scheme |

What is the Voluntary Provident Fund (Vpf)?

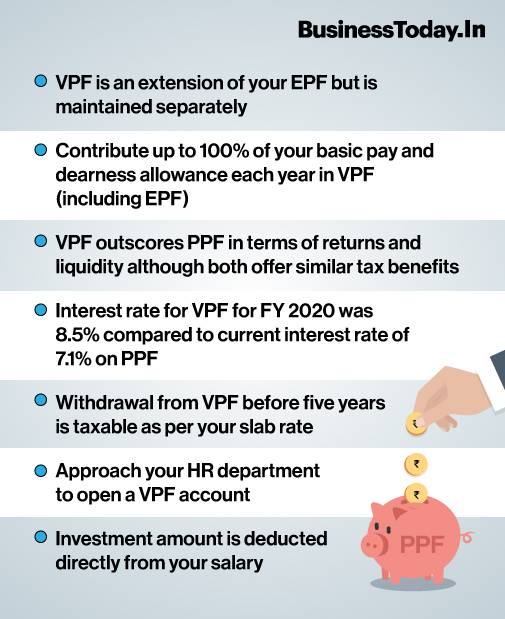

- The Voluntary Provident Fund is a retirement savings scheme available to salaried employees who are already contributing to the Employees’ Provident Fund. Under EPF rules, employees must contribute 12 percent of their basic salary and dearness allowance each month. VPF allows employees to voluntarily increase their contribution beyond this mandatory limit. The major attraction of the scheme is that additional contributions also earn the same VPF rate at 8.25%. This means employees can significantly increase their retirement savings while earning stable returns over time.

- Another advantage of VPF is its automatic contribution system. Once an employee opts for it, the chosen amount is deducted directly from their salary every month. This disciplined approach ensures consistent savings without requiring manual investment decisions. Because of the reliable VPF rate at 8.25%, many employees consider it one of the safest long-term wealth-building tools available in India.

Why The Government Kept The Rate Unchanged

The decision to maintain the VPF rate at 8.25% reflects a careful approach by policymakers. Retirement schemes must balance attractive returns with long-term sustainability.

Several factors likely influenced the decision.

Protecting Retirement Savings

Provident funds are designed to support individuals after retirement. A stable interest rate ensures that employees receive predictable returns and are protected from sudden economic fluctuations.

Economic Conditions and Interest Rate Cycles

Interest rates in government-backed schemes are often influenced by broader economic conditions. By keeping the VPF rate at 8.25%, authorities aim to provide competitive returns while maintaining the financial health of the provident fund system.

Maintaining Confidence In Provident Fund Schemes

Millions of salaried workers rely heavily on EPF and VPF as their primary retirement savings. Any sudden drop in interest rates could affect confidence in the system. Maintaining the VPF rate at 8.25% reassures contributors that their long-term savings remain secure.

Why Investors Are Asking Questions

Despite the stability offered by the VPF rate at 8.25%, modern investors are increasingly evaluating their options more carefully.

Inflation Impact

Inflation reduces the real value of money over time. If inflation averages around 5 to 6 percent annually, the effective real return from the VPF rate at 8.25% becomes relatively modest.

More Investment Choices Available

Today’s investors have access to several alternative investment options such as equity mutual funds, index funds, hybrid funds, and the National Pension System. Some of these options can deliver higher long-term returns, although they carry greater risks.

Changing Investor Mindset

Financial awareness in India has grown rapidly over the past decade. Investors are increasingly looking beyond traditional fixed-income instruments and exploring diversified portfolios that combine both growth and stability.

Key Benefits of Investing in VPF

Despite the growing debate, the VPF rate at 8.25% continues to offer several advantages that make it attractive for long-term investors.

Stable And Guaranteed Returns

One of the biggest benefits of VPF is the certainty it offers. Unlike market-based investments that can fluctuate dramatically, the VPF rate at 8.25% provides predictable annual returns.

Attractive Tax Benefits

- VPF contributions qualify for tax deductions under Section 80C of the Income Tax Act. This allows investors to reduce their taxable income while simultaneously increasing their retirement savings.

- In addition, interest earned remains tax-free within certain limits, making the VPF rate at 8.25% even more appealing for tax-conscious investors.

Long-Term Compounding Growth

- Because the interest is compounded annually, the VPF rate at 8.25% can generate substantial wealth over a career span of 20 to 30 years.

- For example, consistent monthly contributions combined with compounding interest can significantly increase the size of a retirement corpus.

High Safety and Government Backing

The scheme is managed by the Employees’ Provident Fund Organisation and backed by the government, making it one of the safest investment options in India.

Limitations Investors Should Consider

While VPF offers several benefits, it also has certain limitations that investors should keep in mind.

Limited Liquidity

Funds invested in VPF are usually locked until retirement. Although partial withdrawals are allowed in certain situations, the scheme is primarily designed for long-term savings.

Fixed Returns

Unlike equity investments, VPF returns are fixed and do not benefit from stock market growth. Investors looking for higher returns may need to combine VPF with other investment options.

Tax Rules For Higher Contributions

Recent tax rules state that interest earned on employee contributions exceeding a specified limit may become taxable. This affects high-income investors who contribute large amounts to VPF.

Who Should Consider Investing in VPF?

The VPF rate at 8.25% makes the scheme suitable for several types of investors.

Conservative Investors

Individuals who prefer safe and stable investments will benefit the most from the VPF rate at 8.25%.

Long-Term Retirement Planners

Employees planning for retirement decades in advance can use the VPF rate at 8.25% to steadily grow their savings through disciplined contributions.

Salaried Individuals Seeking Tax Savings

People who want to maximize tax deductions under Section 80C often use VPF contributions to increase their retirement savings.

Should Investors Rely Only on VPF?

Although the VPF rate at 8.25% offers strong stability, financial experts usually recommend not relying on a single investment option.

A balanced retirement portfolio may include:

- Provident fund contributions

- Equity mutual funds

- National Pension System

- Debt funds or bonds

This combination helps investors benefit from both safety and long-term growth.

The Big Question: Stability Or Growth?

- The decision to maintain the VPF rate at 8.25% highlights the government’s commitment to protecting retirement savings. For millions of employees, the scheme remains a reliable and trusted investment option.

- However, modern investors are increasingly focusing on diversified portfolios that combine secure savings with higher growth opportunities. The real question is not whether the VPF rate at 8.25% is good or bad, but how it fits into a broader financial strategy.

- For most investors, the smartest approach is to use VPF as a stable foundation while also exploring other investments that can potentially deliver higher returns over the long term.

Read More:-

FAQs

What is the Current VPF Interest Rate in India?

The current VPF rate at 8.25% is aligned with the interest rate declared for the Employees’ Provident Fund for the financial year.

Is VPF Better Than PPF?

VPF often offers a higher interest rate than PPF, but it is available only to salaried employees who are part of the EPF system.

Can I Withdraw VPF Before Retirement?

Partial withdrawals are allowed under specific conditions such as medical emergencies, education expenses, or home purchase.

Is VPF a Safe Investment?

Yes, VPF is considered extremely safe because it is managed by EPFO and supported by the government.